COMPOUND INTEREST: The interest on interest is called compound interest. When the interest at the end of a specified period is added to the principal and the interest for the next period is calculated on the new principal, then it is called compound interest.

Conversion Period: The fixed interval of time at the end of which the interest is calculated and added to the principal at the beginning of next interval of time, is called conversion period. In order words conversion period is the time at the end of which the interest is compounded. If the interest is compounded k times a year then the amount after n years is

and compound interest C I = A - P

![\therefore\:\:\:CI= P\left [ \left ( 1+\frac{r}{k} \right )^{km}-1\right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_917b8b87c0bedd28dc59993e8a85ab11.gif)

| Where, | A = Amount |

| C I = Compound interest | |

| P = Principal | |

| R = annual interest rate | |

| N = Number of years | |

| K = Number of conversion |

If interest is compound annually then k = 1, if half yearly then k = 2, if quarterly then k = 4, if monthly then k = 12, if weekly then k = 52, and if daily then k = 365.

Nominal Rate and Effective Rate: The annual compound interest rate is called the nominal interest rate. When the interest is compound more than once in a year the actual percentage of interest per year is called the effective rate of interest.

| Where | r = nominal rate of interest, |

| K = number of conversations | |

| Also, |  |

| Where | I = amount of interest, |

| E = effective rate of interest in decimal, | |

| P = principal amount, | |

| n = time period. |

Effective rate of interest is always greater than the nominal rate of interest.

Effective rate of interest is not related to the amount of principal.

If the interest rate is  for the first year,

for the first year,  for the second year,

for the second year,  for third year then.

for third year then.

Amount after  year =

year =

Amount after  year =

year =

If V is the value of an item and if R is the rate of depreciation per year then the depreciated value of item after n years is obtained by

When the rate of depreciation is for the first year, for the second year, for the third year then the depreciated value of that item after third year is

ANNUITY: A series of equal and regular payments of a fixed sum of money made at equal interval of time is called annuity. Annuity may be of two types.

Annuity Regular: In this type the first payment or receipt is made at the end of the period.

Annuity Due or Annuity Immediate: In this type the first payment or receipt is made at the beginning of the period.

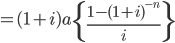

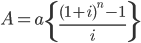

Future Value of Annuity: The amount to be paid or received as an annuity at the end of every fixed period, if the interest is added at compound rate of interest for the next period, is known as future value of annuity. It is the tomorrow’s value of today’s money compounded at the rate value of interest. Thus future value is the cash value of an investment at some time in future . In ordinary annuity each payment is made at the end of each payment period. Then the ordinary annuity of n payments of Rs. a each, where the interest rate is i per period is

![A= A(n,i)= \left [ \frac{(1+i)^{n}-1 }{i}\right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_afea658579d4f3c79af1cadbff78dc03.gif)

In annuity due or annuity immediate the first receipt or payment is made at the beginning. Here the formula for the annuity is

![= (1+i)\cdot a\left [ \frac{(1+i)^{n}-1 }{i}\right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_b9862ae104717b4644b9024c48dd3608.gif)

Present value of Annuity: If the sum paid or received yearly or at an interval of certain period is computed with its present value, naturally the present value is less because of compounded factors. Present value is today’s value of tomorrow’s money discounted at the interest rate. If the annuity is payable or receivable at the end of year (Ordinary annuity) then the formula for present value is

If the annuity is payable or receivable at the beginning of year (annuity due) then the formula for present value is

If the annuity is payable or receivable yearly on payment basis then

If the annuity is payable or receivable half yearly, quarterly, monthly or weekly then all the above formula can be adjusted to find out the present or future value of annuity. In such cases n is replaced by nk and i is replaced by i/k where k is the number of conversations.

SINKING FUND: It is fund created by a company to meet predetermined debts or certain liabilities out of their profit at the end of every accounting year. This fund is also known as pay back fund. This fund is invested elsewhere at a certain rate of interest and the proceeds of such interest is also reinvested again and again . When need arises this fund is disinvested and cash can be used to meet the fixed liability or to replace old units or business. The formula used for sinking fund is

Solved Examples of Compound Interests

Example 1. A person deposited Rs.1,00,000 in his bank for 3 years at simple rate of 6%. How much would be the final value of deposit.

Solution : Here P=100000, n=3, r=0.06

Final value of deposit=P(1+rn)

= 100000(1+(0.06)(3))

= 118000

Example 2. Some part of Rs. 10000 was lent at 8% per year and remaining was deposited in bank at 6% per year. If the total simple interest from both the fractions in 3 years was Rs. 2160, calculate the amount lent at 8% per year.

Solution : Let x be the amount lent at 8% per year. Then (10000 - x) amount is deposited at 6% per year in bank.

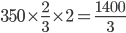

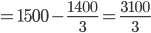

Example 3. A certain sum of money amounts to Rs. 1500 in 2 years and to Rs. 1850 in 3.5 years. Find the sum and rate of interest.

Solution : Simple interest for 1.5 years = (1850 -1500) =350

Simple interest for two years =

Principle

Principle

Now

Rate

= 11.07 %

Example 4. Miss Krupati deposits a sum of Rs.200000 in a bank. After 2 years she withdraws Rs.100000. At the end of 5 years she received Rs.170000. Then find the rate of interest.

Solution : Simple interest on Rs.200000 for 2 years

Simple interest on Rs.100000 for Next 3 years

Now, Interest = 170000 - 100000 = 70000

400000 - 300000r = 70000

400000 - 300000r = 70000

700000r = 70000, r = 0.10

Rate of interest = 10%

Important Questions on Compound Interests

IBPS questions related to Simple and Compound Interests

![Compund \, \, Interest=4500\left [ \left ( 1+\frac{4}{100} \right )^{2}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_1d061937b54d0374c8f9d0b3e1540c8f.gif)

![=4500\left [ \left ( \frac{26}{25} \right )^{2}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_340471e8ea2d717a5e54cd300dfed9d9.gif)

![=4500\left [ \frac{26^{2}-25^{2}}{25^{2}} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_f8c417132737a10c6b2b17df62ddda07.gif)

![=4500\left [ \frac{\left ( 26-25 \right )\left ( 26+25 \right )}{625} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_2775c53b194c630da98af894af9d77f3.gif)

![=4500\left [ \frac{\left ( 1 \right )\left ( 51 \right )}{625} \right ]=Rs \, \, 367.20](https://questionpaper.org/wp-content/plugins/latex/cache/tex_456e1a4a239fea02bb38a02d7aab6880.gif)

![Compund \, \, Interest=4800\left [ \left ( 1+\frac{6}{100} \right )^{2}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_51cfd025a620e0c1bca6dc9c97d48bdf.gif)

![=4800\left [ \left ( \frac{52}{50} \right )^{2}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_a93ff17c7a7d93234f4ec48235360d41.gif)

![=4800\left [ \frac{53^{2}-50^{2}}{50^{2}} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_415c7eac8ac272c14b909b656551b309.gif)

![=4800\left [ \frac{\left ( 53-50 \right )\left ( 53+50 \right )}{2500} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_0d7975a878391755897e8389609bf878.gif)

![=4800\left [ \frac{\left ( 3 \right )\left ( 103 \right )}{2500} \right ]=\, \,Rs \, \,593.28](https://questionpaper.org/wp-content/plugins/latex/cache/tex_94f58341cab6bc82aa6af94d2cd4d8ff.gif)

![Compund\,Interest=2000\left [ \left ( 1+\frac{15}{100} \right )^{3} -1\right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_98a77ea69ecc7335a28a82521e775a8f.gif)

![=2000\left [ \left ( \frac{23}{20} \right )^{3}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_457c9f3f609b31186c25a071b9747385.gif)

![=2000\left [ \frac{23^{3}-20^{3}}{20^{3}} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_85560ad545e505044afc8cb87c13853d.gif)

![=2000\left [ \frac{12167-8000}{8000} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_8a4b3d93ca7473c3b893556bc3008866.gif)

![=2000\left [ \frac{4167}{8000} \right ]=\,Rs\,1041.75](https://questionpaper.org/wp-content/plugins/latex/cache/tex_7a46c69cee93d6ecf5137f84fdf375be.gif)

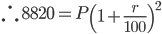

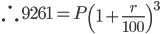

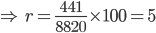

![\therefore 101.50=x\left [ \left ( 1+\frac{3}{100} \right )^{2}-1 \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_4c3822b86ab7b6ea7f0ff0770532acc6.gif)

![\Rightarrow \frac{1015}{10}=x\left [ \frac{103^{2}-100^{2}}{10000} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_cdf0fee0a565796840912ab98f5bb593.gif)

![\Rightarrow \, \, 25220=x\left [ \frac{20}{21} +\left ( \frac{20}{21} \right )^{2}+\left ( \frac{20}{21} \right )^{3}\right]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_670b2100a760c25be82c46f3f9520f91.gif)

![\Rightarrow \, \, \, 25220=x\left ( \frac{20}{21} \right )\left [ 1+\frac{20}{21}+\frac{400}{441} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_2afb533c40bc251cfb7f355adf085aea.gif)

![\Rightarrow \, \, \, 25220\times \frac{21}{20}=x\left [ \frac{441+420+400}{441} \right ]](https://questionpaper.org/wp-content/plugins/latex/cache/tex_7f9fe9a34003684592e4e2d6c65a8f46.gif)

0 Comments